The US Dollar is the least popular reserve currency, except for all the others

The greenback’s share of global trade and central bank reserves is decreasing. However, no convincing alternative has established itself, despite efforts by BRICS countries.

Lesen Sie die deutsche Version hier.

The US dollar has served as the global economy’s main reserve currency since the culmination of World War II, and remains the most extensively utilized currency for international trade. Robust worldwide demand for the USD enables the United States to avail itself of inexpensive credit due to low bond yields, and to utilize the currency for diplomatic purposes. However, the widespread application of financial sanctions as an instrument of foreign policy by the US has prompted some nations to seek means of trading in alternative currencies – a phenomenon called de-dollarization.

Since the outbreak of the Ukraine War in February 2022, for instance, Russia has been subjected to the strictest global sanctions regime ever by the West, led by the US. Curbs have been implemented to restrict Moscow’s access to the international financial system and bank accounts required to finance the Kremlin’s war machine. Export restrictions were also applied to curb Russia’s ability to import goods required to arm a contemporary military, like computer chips. More than 30 countries including the US, the UK, Canada, Australia, Japan, and the states of the European Union are partaking in this unmatched penal regime, applying price ceilings on Russia’s energy exports, freezing Russian Central Bank assets, and curbing Moscow’s access to SWIFT – the foremost international financial transfer apparatus.

In fact, it is because of Russia’s resilience despite these stringent financial sanctions and India’s ongoing reliance on Russia for its defence and energy needs, that New Delhi maintains relations with sanctions-afflicted Moscow.

Russian gas for Europe, Russian oil for India

Notably, the Russian economy’s gross domestic product (GDP) has increased by 5.4 per cent year-over-year in the first quarter of 2024, in line with its flash estimate, after rising by 4.9 per cent in the last quarter of the previous year. The growth uptick continued the robust momentum in GDP after last year’s recovery from the 2022 crash, albeit relying heavily on state-financed investment in arms and ammunition.

The output expansion was supported by wholesale and retail trade (11.4 per cent), manufacturing (9 per cent), as well as construction (4.8 per cent). Russia’s economic construct has also supported its economic growth amid the prevailing sanctions. Largely unaltered from the Soviet era, state-owned enterprises contribute approximately two-thirds to the country’s GDP, whereas small and medium-sized companies account only for a fifth of GDP. Though this construct may not appear conducive to economic growth, it can act as a stabiliser during adverse circumstances, as was witnessed during the Covid-19 lockdowns.

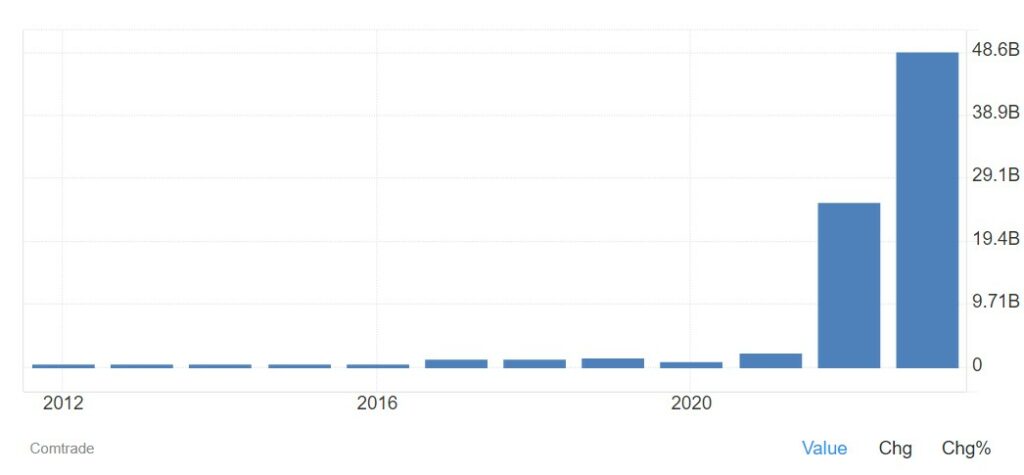

Interestingly, Russia has also been able to sustain its liquefied natural gas exports to Europe. Consequently, New Delhi feels validated in its imports of Russian oil despite widespread Western sanctions on Moscow, as well as Western pressures to curb these purchases (see Figure 1).

Figure 1: India’s crude oil imports from Russia (2012-2023).

Source: Trading Economics

New Delhi has also expressed its intent to sustain its purchases of Russian crude oil near or above the USD 60-a-barrel price ceiling imposed by the G7 as it negotiates external economic uncertainties, prompting speculation regarding the implications of such USD-independent trade on the American currency’s status as the primary global reserve currency.

Non-traditional reserve currencies benefit

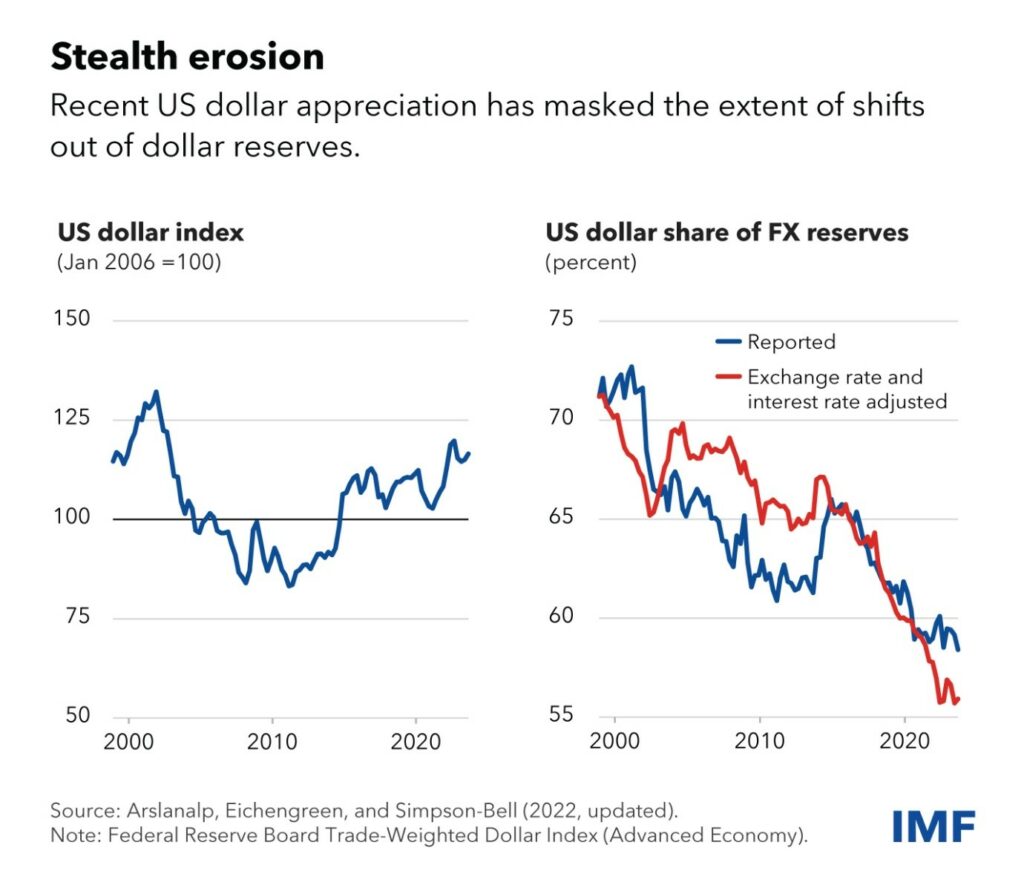

Indeed, recent data from the International Monetary Fund’s Currency Composition of Official Foreign Exchange Reserves (COFER) indicate a continuing steady decrease in the fraction of foreign exchange (forex) reserves allocated by central banks and governments to the USD. The diminished role of the USD over the last two decades, however, has not been to the advantage of the other “big four” currencies – the euro, yen, and pound. Instead, non-traditional reserve currencies including the Australian dollar, Canadian dollar, Chinese renminbi, South Korean won, Singaporean dollar, and the Nordic currencies, have benefitted from the retreating USD. These non-traditional reserves have been attracting reserve managers due to benefits related to diversification and increased liquidity (often driven by novel digital financial technologies) as well as relatively attractive yields.

The shift toward these currencies is especially conspicuous given the USD’s strength, possibly indicating the movement of private investment into USD-denominated assets (see Figure 2). Concurrently, this inference highlights that exchange rate variations can exert a distinct effect on the constitution of central bank reserves.

Figure 2: USD index and the currency’s share of allocated forex reserves of central banks and governments over time.

Source: IMF

On the other hand, statistical tests do not substantiate an accelerating reduction in the greenback’s reserve share, contradicting assertions that US sanctions have hastened migration away from the USD. Although it is possible that the countries looking to shift away from the USD due to geopolitical motivations do not disclose data on the constitution of their reserve portfolios to COFER, the 149 reporting economies account for almost 93 percent of global forex reserves, implying that non-reporters only hold a very minor fraction of global reserves.

The practical problems of a BRICS currency

With its bid to spearhead the development of the BRICS currency, Moscow has sought to increase attention toward the optics surrounding the sustainability of the USD’s dominance. However, the Kremlin’s recurring use of deception as a tool of statecraft evokes suspicion regarding Russia’s steadfastness toward the goal of a shared BRICS currency. Currently, ambiguity exists on multiple practical issues.

«The Kremlin’s recurring use of deception as a tool of statecraft evokes suspicion regarding Russia’s steadfastness toward the goal of a shared BRICS currency.»

A difficulty is that the BRICS is not an especially strong economic bloc. It attempts to amalgamate economic behemoth China with emerging India and three significantly smaller commodity export-dependent economies. Infeasible as a monetary union, the BRICS constituents are very different in respect of international trade, economic growth, and global integration of capital markets. More crucially, China’s economic heft and increasing influence over Russia entail that as a potential USD alternative, the BRICS currency does not represent a varied bloc of growing economies but a single domineering country, China – a gigantic blotting paper for energy and other raw materials.

Despite its clout, though, Beijing has proven incapable of establishing even the renminbi as a feasible substitute to the USD, let alone a BRICS currency. This is partly because successfully internationalizing the renminbi depends on Beijing’s cost-benefit analysis, and the need for its economy’s share in global production and trade to be high enough. Moreover, the renminbi is not sufficiently trusted globally because Beijing strictly regulates capital transfers as well as domestic financial markets. For that matter, even the Indian rupee can only be internationalized incrementally, as India’s financial markets deepen gradually, and the RBI would want to ensure sufficient forex reserves before implementing full capital account convertibility.

The editor-in-chief of Forbes magazine, Steve Forbes, has argued that there are symptoms of the world starting to stagger toward a gold-based monetary architecture including record central bank purchases of gold in recent years and experimentation with gold-based government bonds. However, this rise in official gold demand is not as unprecedented as occasionally projected, with gold having reversed the erstwhile decline in its fraction of official foreign reserves more than a decade ago. The increase in demand has only elicited excitement due to having occurred against the background of a prolonged fall in the proportion of global reserves held in the form of gold, extending over almost four decades, and is certainly nowhere close to ridding the USD of its global reserve status.

Sanctions-proofed trade

To the extent that there are countries attempting to trade in currencies other than the USD, de-dollarization is not a myth. For instance, India and Russia have been attempting to sanctions-proof their trade from Western sanctions by inter alia discarding the USD as a medium of exchange, and have arguably met with significant success.

USD appreciation in recent years has disguised the magnitude of out-migration from USD-denominated central bank reserves globally, with the greenback mostly being replaced by non-traditional reserve currencies. Yet there is no credible empirical evidence of an accelerated reduction in the USD’s share of global reserves, in part because no convincing and trusted global reserve alternative to the USD exists.

The greenback therefore looks set to remain the world’s primary reserve currency unless Washington recklessly weaponizes it as an instrument of financial sanctions on a significantly larger scale.